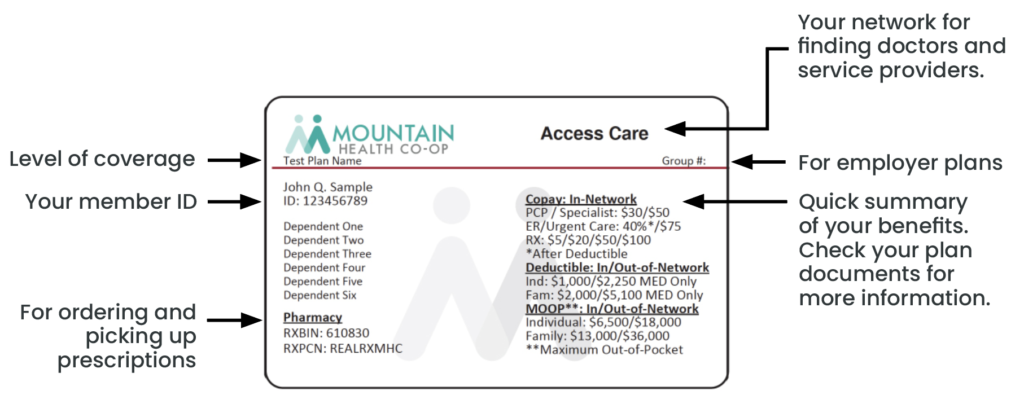

Members

Maximizing your coverage

Avoid unexpected costs by understanding what’s covered under your plan.

Get paid up to $210 per year.

You don’t have to meet your deductible, or any other requirements, to use these perks.

Our Individual and Group plans include Signature Benefits that let you immediately save money.

#1 way to always save

Use In-Network providers as much as possible.

Inquire about services before they’re performed to confirm that every provider involved in your treatment is In-Network.

Be aware that even if you see a provider in your network, they may use an out-of-network provider for some services such as routine lab work.

Ask prior to receiving these services or you may receive a bill for the difference (balance billing) if the situation was not an emergency.

Find In-Network Doctors

to keep costs lower.

Is this covered?

Confirm coverage for procedures or services ahead of time to save money.

Step 1

Request the CPT code (Current Procedural Terminology) from your provider.

These unique 5-digit codes identify the procedure anywhere in the United States.

Step 2

Search for your code to see if it requires preauthorization.*

If so, your provider will take the next steps to request authorization.

* The search tool doesn’t include pharmacy services and products. For pharmacy prior authorization: Pharmacy Services and Products requiring Prior Authorization

Check coverage by phone.

Still wondering if a service is covered? Get your CPT code and call Member Services to confirm: 800-299-6080

In-Network

You will receive the highest level of benefits and coverage when you see an in-network provider.

You will not be billed for balances on covered services beyond any copayment, deductible, and/or coinsurance.

Our in-network providers automatically submit claims to us on your behalf so you don’t have to do anything.

Out-of-Network

If you choose an out-of-network provider, your coverage may be lower. You will likely pay more directly and may need to submit a claim yourself.

When you receive services from an out-of-network provider, you may receive a bill for the difference between what the CO-OP considers payable and the provider’s charges.

This is called balance billing, and you’re responsible for paying the remaining balance if you voluntarily choose the provider.

This is different than Surprise Billing protection because the provider was chosen voluntarily.

Out-of-Network Maximum

Be aware that costs from out-of-network providers may go beyond your maximum out-of-pocket limit because they can charge you more than what your insurance covers.

Any excess amounts won’t count towards your out-of-network deductible or maximum out-of-pocket.

Avoiding unexpected costs.

Be aware that even if you see a provider in your network, they may use an out-of-network provider for some services such as lab work or imaging diagnostics.

Ask prior to receiving these services or you may receive a bill for the difference (balance billing) if the services weren't urgent.

Emergency Care & Surprises

Your plan level will determine hospital coverage and costs. Details of which can be found on your Summary of Benefits document.

However, it is not uncommon to hear stories of people having an emergency situation only to be stuck with high bills once everything is over.

This practice is known as surprise/balance billing and can occur when you are treated at an out-of-network facility or provider or have ancillary services performed by an out-of-network provider at an in-network facility.

We do not allow Balance Billing for emergency situations.

You are protected.

Balance billing is no longer allowed with our plans for emergency or surprise situations.

If you are ever balance billed in an unexpected emergency situation, please call us immediately. You have coverage after normal business hours for non-emergency care.

Protection is only for emergency scenarios and does not cover voluntarily chosen out-of-network providers.

Balance Billing Example

John had a climbing accident that shattered his leg. Once at the hospital, he required immediate reconstructive surgery.

Afterward, he discovered that the hospital’s anesthesiologist was not in his plan’s network, despite being at an in-network hospital.

Since it was an emergency, he couldn’t control who was involved in his care.

John was protected from Surprise / Balance Billing so he didn’t need to pay the out-of-network fees at his in-network hospital.

Smartest Way to Save Long Term

Visit your Primary Care Provider regularly.

Seeing the same doctor regularly can help identify underlying health conditions before they become serious.

Many plans include low or $0 co-pay visits to a Primary Care Provider (PCP). Check your documents for full details.

You may choose any of the following types of providers as your primary care physician:

Family Practice, Internal Medicine, Pediatrician, Obstetrics and Gynecology, Gynecologist, Geriatrician, Osteopath, Nurse Practitioner, and/or Physician’s Assistant.

Remember to choose an in-network PCP.

Find a Primary Care Provider.

Take advantage of all your plan’s preventive perks.

Preventive Care Benefits

Mountain Health CO-OP is here is to help you understand the list of screenings, medications, and vaccinations that are 100% covered just for you.

You pay nothing*.

It’s that easy.

If you are enrolled in a Mountain Health CO-OP Insurance Plan, you are eligible for 100% coverage for wellness or preventive services*.

To learn more about your preventive benefits, call the number on the back of your ID card to talk to a customer service agent about your benefits.

Services that are listed in your member benefit plan under “preventive health benefits” are covered at 100%*.

This means that you have no out of pocket cost. You do not have to pay a copay, deductible, or co-insurance to have these services done when you see an in-network doctor, laboratory, hospital, or durable medical equipment provider.

You may have to pay your deductible, copay, and coinsurance if you choose to have these services by an out-of-network doctor, laboratory, hospital, or durable medical equipment provider.

If you need help finding an in-network doctor, call the number on the back of your ID card, and Customer Service can help you. Or search for a provider.

Preventive care is the health care that you get to prevent illness, detect medical conditions, and keep you healthy.

For example, your doctor might want you to get a colonoscopy because of your age. However, if your doctor wants you to have a colonoscopy because of you are having symptoms like diarrhea or stomach pains, this is diagnostic care.

The diagnostic colonoscopy would not be paid under your preventive benefit, and you would be responsible for coinsurance, copayments, and your deductible.

Remember to ask your doctor if tests and procedures are preventive or diagnostic and if they are in-network with Mountain Health CO-OP.

Your annual wellness exam is one of the many preventive services that the CO-OP covers at 100%. However, some of the tests or procedures your doctor orders may not be covered under your preventive health benefit or your benefit plan.

If you have any questions about benefit coverage, call the number on the back of your ID card, and Customer Service can help you.

Mountain Health CO-OP supports federal and state government mandates to cover a wide range of preventive services. The CO-OP follows recommendations from government agencies to determine which services we include.

These recommendations can change, and the CO-OP regularly updates your benefits to reflect evidence-based practices. The CO-OP may adopt or change covered preventive service guidelines within the time required by law. Visit uspreventiveservicestaskforce.org/ for more information.

There are many reasons why you may have received a bill for a visit. You may have seen an out-of-network doctor, the doctor may have billed MHC with codes that told us you were there for something other than an annual preventive exam, or the tests or services you had done were not covered by your health plan.

If this has happened to you, call us at the number on the back of your ID card and we can help you understand your bill.

Care Management

Get a free health assessment

in your home.

Our care management teams help members get the right care at the right time for the best outcome using evidence-based guidelines.

We offer you the opportunity to complete a free, confidential and voluntary health risk assessment (HRA) to see how healthy you are.

- Free Health Assessment

- Get Help with Health Conditions

The HRA identifies personal risk factors and provides an action plan to help prevent future conditions or manage current conditions.

This program entitles you to work one-on-one with a nurse care manager. It is our goal to assist you in getting the best possible health care.

Get a free health assessment

in your home.

Fine print

*Preventive Health Care services are covered at 100%, with no out of pocket costs when contracting provider networks are used. Any services performed with an Out of Network Provider will result in copayments, deductibles, and cost-sharing and may result in balance billing. Your doctor must write a prescription for preventive medication services to be covered by your plan, even if they are listed as over the counter.

MHC complies with applicable Federal civil rights laws and does not discriminate on the basis of race, color, national origin, age disability, or sex.

** This is a reimbursement program. See Benefits page for further details.

Reading your Plan

Avoid unexpected costs by reading your plan closely.

Double check coverage and equip yourself with knowledge when it comes to reading plan documents.

How to maximize your health plan.

Understanding your plan documents

Summary of Benefits and Coverage (SBC)

For most people, this will probably be the most important document to examine when comparing plans and understanding coverage options.

The SBC summarizes how your plan shares the costs for covered health care services. This is a summary of the legal requirements found in the Policy.

Key Details:

- Brief descriptions of limitations, exceptions, and other important details

- Deductibles

- Copays

- Coinsurance

- More in depth than the OOC

Outline of Coverage (OOC)

A brief description of the important features of your policy. This is not the insurance contract and only the actual policy provisions will control.

Key Details:

- Outlines the plan’s in-network and out-of-network costs

Policy

This is a legally binding contract between us, the insurance company, and you, the policy holder.

It details the rights and obligations, of both you and those of Mountain Health Co-Op.

Key Details:

- Highly detailed explanations

- Explains prior authorization requirements

- Lists all excluded benefits

- out-of-network options

Explanation of Benefits (EOB)

This is not a bill. The EOB breaks down your bill details between the medical service provider(s), Mountain Health CO-OP, and you.

Key Details:

- Services provided

- What the doctor or hospital charged (all charges)

- What insurance covered

- What your insurance agreed to pay

- The amount you must pay (amount you are responsible for)

Help with Health Conditions

New health changes and preexisting conditions — like asthma or diabetes — can be overwhelming.

Discover resources to help manage complications and minimize costs.